Risk & Return

25 January 2023

Hi, The Investor’s Podcast Network Community!

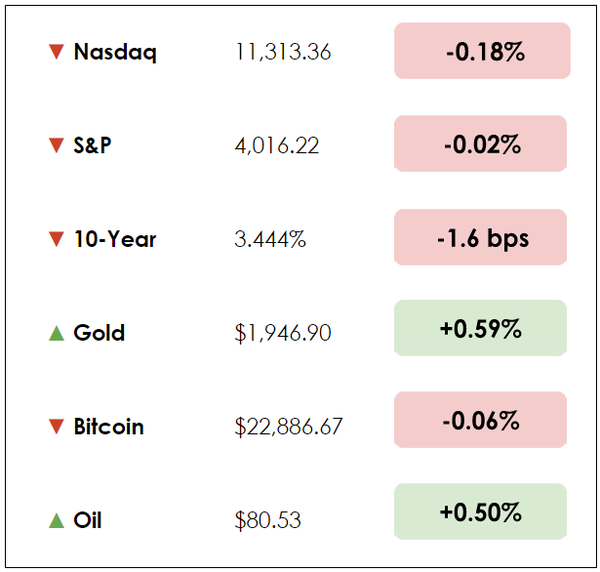

Stocks were in the red most of the day but rose into the close to finish about flat.

Microsoft (MSFT), which kicked off big-tech earnings on Tuesday, posted slowing sales growth, though its earnings beat Street estimates.

Earlier, Tesla (TSLA) reported record revenue ($17.72 billion) and an earnings beat on both the top and bottom lines 🚗

Meanwhile, Canada’s central bank signaled it would pause subsequent interest-rate hikes, the first major central bank to do so. Perhaps more will follow soon?

Here’s the market rundown:

MARKETS

*All prices as of market close at 4pm EST

Today, we’ll discuss two items in the news: Wall Street meets music streaming and tech startups targeting the human brain, plus our main story on understanding risk.

All this, and more, in just 5 minutes to read.

Understand the financial markets

in just a few minutes.

Get the daily email that makes understanding the financial markets

easy and enjoyable, for free.

IN THE NEWS

🎶 A Chance to Invest in Music (FT)

- Investors may soon be able to speculate on which songs will top music charts, as the Chicago-based start-up Clouty intends to launch a futures market tied to music revenues. Clouty has created a tradable index of global streaming sales, and it’s considering an exchange-traded fund (ETF) for individual investors to access.

- The company is also in early discussions with U.S. exchanges about launching futures contracts related to individual genres, artists, and songs. Its Musiq 500 index tracks revenues generated by the top 500 songs globally, and its value has already risen more than 25% in the past year.

- Skeptics question whether Clouty can attract big institutional investors and market makers, though, whose daily buying and selling build liquidity. One expert remarked, “There have been many instances of futures that have failed to succeed, even on well-understood products. They’re usually too complex to understand or too complex to price.”

- In recent years private equity groups like Blackstone and KKR have spent billions of dollars on catalogs for artists like Neil Diamond and Bruce Springsteen, hoping that these can provide stable, recession-proof income streams. Clouty’s chief executive says, “Music is an asset class that’s hiding in plain sight and hasn’t been unlocked.”

- Goldman Sachs predicts that global music industry revenues will grow at a compounded annual rate of 12% through 2030, hitting over $150 billion. With this growing space inevitably comes investor demands to trade music rights on secondary markets.

- For streaming platforms like Spotify, YouTube, and Apple, a futures market could enable them to hedge risks associated with rising costs for song licensing.

🧠 Tech Startups Target the Human Brain (Bloomberg)

- A new brain science company co-created by Benjamin Rapoport, a founding member of Elon Musk’s Neuralink, is raising millions to construct small electronic implants inside human skulls.

- Precision Neuroscience Corp. plans to announce that it raised $41 million for brain implants that target neurological disorders such as epilepsy. By placing sensors on top of brain tissue, not penetrating it, the implants are hoped to correct a whole spectrum of conditions. This emerging field of brain-computer interfaces is piquing investors’ interest, raising $274 million last year.

- Neuralink remains the most famous in the sector, with Musk suggesting its technology would enable those with paralysis to control an external machine, like a keyboard, directly from their brains.

- Implanting chips is dangerous, but proponents argue that the potential benefits are worthwhile. Precision’s new funds will help it push through the regulatory process toward its first human implant, which it has only tested successfully in pigs so far.

- The company believes its implant could also treat stroke, dementia, and traumatic brain injuries. And Precision has a serious cast behind it, hiring Alphabet’s (GOOGL) Craig Mermel as chief product officer and Apple’s (AAPL) Dan Trietsch as principal software architect.

- The entire space remains controversial, yet companies continue to advance and secure investor funding. In the coming years, we’ll learn whether brain implant technology can truly live up to its revolutionary promises.

WHAT ELSE WE’RE INTO

📺 WATCH: Principles for building wealth and wisdom with Guy Spier and Mohnish Pabrai

👂 LISTEN: NFL’er has time for real estate, so do you. Real estate 101 with Robert Leonard

📖 READ: Lauren Sanchez on going to space and working with Jeff Bezos

THE MAIN STORY: VOLATILITY IS NOT RISK

“People who succeed in the stock market also accept periodic losses, setbacks, and unexpected occurrences. Calamitous drops do not scare them out of the game.” — Peter Lynch

In a 2006 memo to clients, Howard Marks pointed out that many people talk about returns but few talk about risk-adjusted returns. The same could be said today.

Investors’ returns tell only half the story. We must know how much risk they took to generate those returns before we can tell whether they did a good job.

As Marks wrote 17 years ago, there’s a misconception that, especially in good times, “‘Riskier investments provide higher returns. If you want to make more money, the answer is to take more risk.’” But riskier investments absolutely cannot be counted on to deliver higher returns. Why not? It’s simple: if riskier investments reliably produced higher returns, they wouldn’t be riskier!”

In this edition, we’ll explore some basics of risk, risk management, and how to confront it.

Improbable things happen all the time

Investing involves dealing with the future. The challenge? The future is inherently uncertain. Thus, risk is inescapable.

Investors must face it head-on. While many investors shy away from risk, it’s what makes the whole game of investing interesting. A job without challenge is boring.

For a challenge to be present, there must be risk.

Let’s say you make an investment you consider risky. Maybe you buy a stock at $100 today and sell it next year at $200. Was it risky? It depends.

Maybe the investment was exposed to many risks that didn’t materialize. Or maybe you bought another stock at $100, which fell to $50 when you sold, marking a 50% loss.

Does that mean it was riskier than the other investment? Not necessarily. The fact that something happened doesn’t mean it was bound to happen.

Probable things fail to happen – and improbable things happen – all the time.

You can’t predict risk

In short, return alone says little about the quality of investment decisions. Risk, defined as the possibility of financial loss, is integral to understanding the quality of a decision. The issue?

You can’t predict risk, which makes it hard to recognize, especially when emotions are running high. It’s truly only seen in retrospect.

Risk is highly subjective and difficult to measure. Volatility is more straightforward and measurable because it’s merely the standard deviation of returns. So, the terms are sometimes used as if they were interchangeable.

In bullish times, human psychology leads many investors to overestimate their ability to see risks. The prevailing wisdom is that risk increases in recessions and falls in booms.

In contrast, it may be more helpful to think of risk as increasing during upswings, as financial imbalances build up, and materializing in recessions, noted Andrew Crockett, a British banker, and economist.

Because of investor psychology, markets generally swing toward or back from one extreme or the other. Marks has said that participating when prices are high rather than shying away is the main source of risk.

Risk intelligence

A key passage from Marks’ memo? Diversification vs. concentration.

Concentration is widely seen as risky, but it’s not if you know what the future could hold. For focus investors who can foresee the growth of a business, concentration can maximize return, and diversification can hold it back.

Investor A could have a relatively concentrated portfolio of five businesses, while investor B might hold 40 businesses. Yet investor A’s portfolio could be less risky if the investor manages it superbly and understands the exposures.

Investor B could be diversified but still susceptible to enormous risk.

Marks writes that his risk memo was prompted by a Rick Funston quote: “You need comfort that the risks and exposures are understood, appropriately managed, and made more transparent for everyone…This is not risk aversion, it is risk intelligence.”

Dive deeper

Howard Marks, back in 2006, writes brilliantly on risk. His memos are evergreen, meaning they could be read and applied to any period, and this is no different.

Happy reading!

SEE YOU NEXT TIME!

That’s it for today on We Study Markets!

See you later!

If you enjoyed the newsletter, keep an eye on your inbox for them on weekdays around 6pm EST, and if you have any feedback or topics you’d like us to discuss, simply respond to this email.